What is Peer to Peer (P2P) Lending

"Peer to Peer lending (P2P lending) connects verified individuals to borrow and lend money online without going to a traditional financial institution. This helps the borrowers get personal loans online at attractive interest rates and helps the lenders for substantial financial growth.

The P2P lending process is entirely paperless. Borrowers can avail P2P loan to fulfill a whole host of their needs. For example, a salaried borrower can get any of the special purpose loans which include wedding loan, medical emergency loan, travel/holiday loan, car loan, used car loan and down payment home loan among others. A business / self-employed borrower, on the other hand, can take working capital loans, equipment financing loans, business expansion loans and inventory/stock purchase loans to name a few, besides all other loans that can be availed by a salaried borrower.

-

Lenders

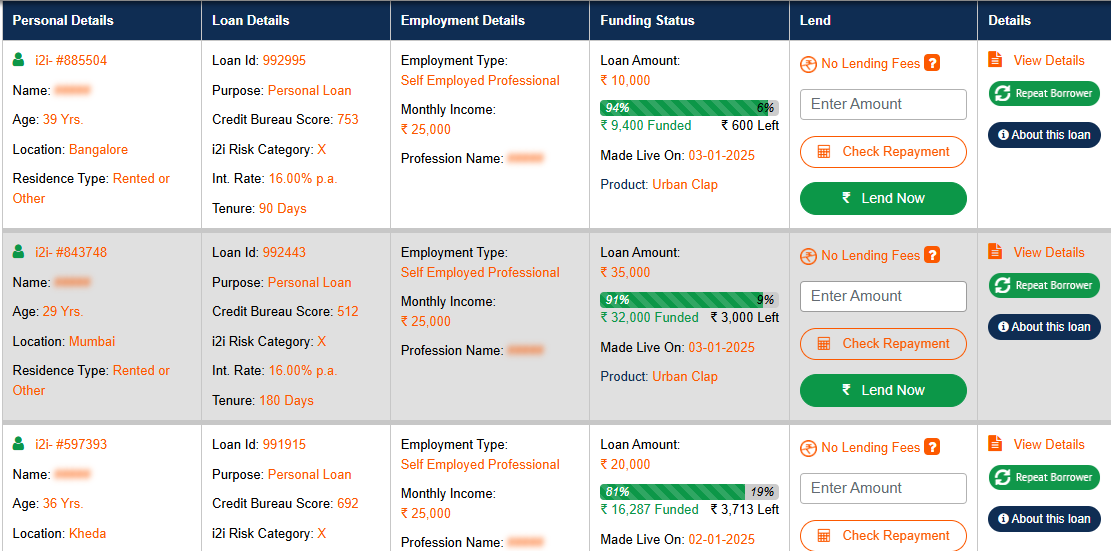

Lenders looking to earn handsome returns can lend money to verified borrowers listed on our website.

-

i2ifunding

i2i performs detailed credit evaluation of borrowers before approving the loan proposal and handholds them throughout the loan cycle—right from the approval stage to the repayment stage.

All transactions are executed through the Escrow account, supervised by the SEBI-approved trustees. -

Borrowers

Individuals can take personal loans on our platform through a hassle-free online process.

Lenders may earn handsome returns which often exceed the returns made on other Lending avenues such as savings accounts, fixed deposits, corporate bonds etc. It is not easy for common lenders to make money through equity markets as it requires constant monitoring and detailed analysis of company financials and business plan. This makes P2P lending a unique Lending option to earn higher returns and puts it firmly as an alternative Lending class. It will help lender attain greater diversification for their overall Lending across stocks, mutual funds, fixed deposits, bonds etc.

Why Borrowers Take Loans at P2P Lending Platform

Irrespective of borrower's creditworthiness, obtaining an unsecured loan from banks is never painless unless you have an excellent transaction history with them. Lengthy paperwork and inflexibility of banks in many areas affect borrowers. Banks don’t offer concessional rates even if the borrower has an excellent credit profile. Moreover, banks reject a loan to borrowers with no or inadequate credit history, no matter how much interest they are ready to pay.

…So there’s a gap.

Peer-to-Peer lending platforms help bridge this gap.

NBFC-P2P Certificate of Registration (CoR) No. : N-12.00468

Why Lend at i2iFunding?

Peer to peer lending is fast becoming a favorite alternative Lending option for lenders seeking higher returns with moderate risk across the major countries of the world such as the US, UK, China and Australia. These countries have led the growth of P2P lending as an attractive Lending avenue. When we compare P2P lending with other Lending options available on different parameters, it clearly emerges as an attractive Lending alternative.

-

Fixed Income

Fixed Income

-

Gold

Gold

-

Equity

Equity

-

Property

Property

Among these four major asset classes, fixed income assets are considered the safest. Although this is true, it’s a misconception that all fixed income assets offer equal safety. Many lenders often make a common mistake—they just compare returns offered by various Lending propositions before lending. While doing this, one can’t forget about the risk involved in any Lending avenue. Lending in Unregulated deposit schemes and Collective Lending Schemes can be very risky as witnessed from time to time. Multiple such schemes have ended up in scandal leaving lenders bereft of their hard-earned money.

In addition, some such as debt mutual fund doesn’t provide a fixed income stream and expose lenders to a moderate to high level of risk.

Fixed income assets that do not have a fixed cashflow

- Debt mutual funds

Fixed income assets that offer you a fixed coupon

- Fixed deposits

- Bonds and Debentures

- P2P Lending

| Various fixed income lending avenues | Returns Range | Risk involved | |

|---|---|---|---|

| Bank Fixed Deposits* | 7.50% | 10.00% | Low |

| Unsecured company fixed deposits* | 7.50% | 13.00% | Medium-High |

| Secured Non-Convertible Debenture* | 8.50% | 12.00% | Medium |

| Unregulated deposit schemes# | 12.00% | 36.00% | High-Very High |

| Debt Mutual Funds** | 7.50% | 9.00% | Medium-High |

| Collective Lending Schemes# | 20.00% | 30.00% | High-Very High |

| P2P Lending | 12.00% | 30.00% | Medium-High |

India’s retail inflation has stayed in the range of 3.69% and 11.16% over the last 10 years and significantly eats into already low returns made in fixed deposits and corporate bonds. This makes P2P lending an attractive proposition as it may help lenders earn higher returns.

Only comparable lending is an lending in stocks. However, this requires patience as one may need to wait for several years for returns. Consider a situation where you do not want to liquidate your lendings as stock markets are terribly down but you need money. Had you Lent in P2P loans, the monthly cash flows could have easily provided you some respite and helped you tide over the situation. P2P lending can add “liquidity certainty” to your portfolio. Considering all these factors, we believe P2P lending is a good choice for smart lenders and provides an attractive lending alternative.

P2P Lending - An Opportunity to Earn High Returns

Lenders may make anywhere between 12-30% p.a. by lending money to verified borrowers through Peer to Peer lending platform like i2iFunding. Lenders can start an lending with as low as Rs. 1,000 and can lend money to multiple borrowers thereby diversifying their lendings.

Interest rates on loans depend on the risk category of the borrower. At i2iFunding, this is determined by our proprietary automated credit evaluation model which considers more than 100 parameters and thousands of data points.

Returns earned by lenders may vary depending upon their risk appetite and lending strategy. A disciplined lender has a good chance of generating handsome returns through a highly diversified portfolio.

Based on historical data, an average diversified lender can make about 18% - 22% p.a. after considering the default risk involved in the high return - low-risk loans.

Wondering why P2P has a high risk-reward ratio?

P2P platforms offer you tremendous flexibility and transparency. For this reason, they are your trusted friend. When you lend in debt funds, you have no control over how is it utilized. At i2iFunding, it’s you who decides whom to lend and how much to lend. i2iFunding offers you a complete analysis of the borrower's credit profile which helps you understand the risk involved and take an informed lending decision.

Diversify your lending and reduce risk exposure

i2iFunding lists loans for multiple purposes which can vary from special-purpose unsecured financial loans to small business loans.

We also classify loans in six categories from A to F—A being the safest and F being the riskiest. Higher the risk, higher is the rate of interest.

You should diversify the lending in terms of both loan purpose and risk category by lending a smaller amount of money in each loan. Since i2iFunding lists a number of loans on a daily basis, you will get ample opportunity to deploy the money. There is no benefit in lending a large amount of money in one loan, it is better to lend the smaller amount in multiple loans.

Adequate diversification across and within categories should help you improve your risk-reward ratio.

Smart Lending Reviews

Your reviews motivate us and help us make our service even better

What customers say about Smart Lending

Suppose you lent Rs.20,000 in five different loan projects with various risk profiles.

| Amount lent (Rs) | Risk Category | Rate of interest | Loan tenure |

|---|---|---|---|

| ₹ 20,000 | B | 15% | 2 years |

| ₹ 20,000 | C | 19% | 2 years |

| ₹ 20,000 | D | 22% | 2 years |

| ₹ 20,000 | E | 24% | 2 years |

| ₹ 20,000 | F | 30% | 2 years |

| ₹ 1,00,000 | 22% | 2 years |

In the above example, your weighted average interest rate comes to 22%, which is fantastic. Isn’t it better to lend in five different loan projects as given above rather than lending in just one?

You can spread your risk further by lending in more than a project in each category.

Suppose you have Rs 20,000 to lend in risk category D, you can lend Rs. 5,000 each across 4 different borrowers instead of one.

All the loan proposals given above belong to the category ‘D’, but each borrower has a different financial background. And all of them differ from one another in occupation and the purpose of borrowing. Their age profiles are also different.

Therefore, lending in four loans in one category will help you achieve further diversification within the category in the real sense.

Do remember—diversification not only reduces the chances of defaults but also allows you to earn significantly higher risk-adjusted returns. Not all of them will default, right?

Higher Liquidity than many other lending options

People looking for regular income mostly lend in Post Office Monthly Income Scheme (POMIS) or in Monthly Lending Plans (MIPs) offered by mutual funds. A few opt for monthly or quarterly options offered by banks etc.

Typically, these products offer limited liquidity options i.e. period for which one can lend and then enjoy the regular monthly income. Also in the case of MIP, the amount of dividend is not fixed.

P2P lending, on the other hand provides adequate liquidity. At i2iFunding, loans typically have tenor from 3 months to 36 months which helps you to manage your liquidity as per your requirements while ensuring a steady monthly income stream to bank on.

| Loan 1 | Loan 2 | Loan 3 | Loan 4 | Loan 5 | |

|---|---|---|---|---|---|

| Interest rate p.a. | 30.00% | 24.00% | 22.00% | 19.00% | 15.00% |

| Tenure of the loan | 24 | 24 | 24 | 24 | 24 |

| Loan amount (Rs) | 20,000 | 20,000 | 20,000 | 20,000 | 20,000 |

| EMI receivable (Rs) | 1,118 | 1,057 | 1,038 | 1,008 | 970 |

| Total EMI receivable (Rs) | 5,191 |

Suppose you lend Rs 1 lakh in the manner above, you would be entitled to receive Rs 5,191 every month for two years.

Unlike that in mutual fund SIPs, endowment life insurance policies and recurring fixed deposits, you do not have any monthly lending commitments. You can set a pace of your lendings . You can lend when you feel you should and for the tenor with which you are comfortable. You can choose interest rate at which you want to lend and can diversify across multiple loans. With so much flexibility, isn’t it a bonanza?.

Smarter Lending Option

P2P lending has clearly emerged as a smarter lending option for your hard-earned money:

- The returns may be higher than what most fixed-income lendings would offer.

- You can generate regular fixed monthly income; making it the ultimate source of passive income.

- You have the option to diversify portfolio based on your risk appetite.

- Liquidate your money every month, or re-lend it on the P2P platform to earn more returns.

Subscribe for the Newsletter

Sign up for the latest updates and offers